Subsidiary in France: which legal status to choose?

When a foreign company wishes to create a subsidiary in France, it can either select the SAS status (French simplified joint stock company), or the SARL status (French limited responsibility company).

The advantages and disadvantages of each status

The SAS is comparable to the incorporated company in English-speaking countries (or the AG in Germany), whereas the SARL is closer to the LLC (English) or the GmbH (German).

The advantages of the SAS status for a subsidiary in France

An SAS has a significantly flexible legal status. It allows the separation of ownership and management. In such a case, the company’s by-laws can enable the formation of a board of directors where all shareholders (operational and non-operational) are represented.

The above-mentioned possibility makes the SAS highly recommended for co-owned companies. In other words, the situation when the foreign company is a shareholder of the French subsidiary alongside another company. The foreign company does not have to participate on a daily basis in the subsidiary’s operations.

A SAS also allows its corporate shareholders to be corporate officers. A SAS does not have to appoint a person as a shareholder corporate officer. This fact provides three benefits on legal and fiscal aspects.

On the legal aspect:

The company appointed as the corporate officer does not need to request for any authorisation. However, for individual shareholders, this situation differs according to the person’s citizenship. Citizens of the European Economic Area do not have to make any demands either. But other citizens who reside in France must request a temporary resident permit (carte de séjour) If the person lives outside of France, authorization from the French authorities (authorisation préfectorale) is required. This authorization can be simple to acquire for North American, Australian and Japanese people, but it can be more difficult for others.

This aspect enables the driving force of the company to be employed by the subsidiary under contract. Henceforth, it would not be liable on commercial law. On the other hand, legal proceedings practices on corporate officers are extremely rare.

Lastly, if the subsidiary only has one shareholder, it is not mandatory to appoint a permanent representative.

On the fiscal aspect:

The appointment of companies as corporate officers significantly eases management fee invoicing and considerably limits the risks of non-deductible costs for the subsidiary. If managers are at the same time a company and a person, a close consideration should be done on the management fees scope to be sure that it does not come in conflict with the person’s responsibilities. This could challenge the cost deductibility of the subsidiary.

The advantages of the SARL status for a subsidiary in France

The main drawback of this status is that you can only appoint a natural person as a corporate officer (no legal entities). As a result, the status is not recommended for subsidiaries. Appointing a natural person as a corporate officer in SARL means the deductibility of the management fees can be easily challenged by tax authorities.

Foreign companies pick SAS over SARL when creating a subsidiary in France

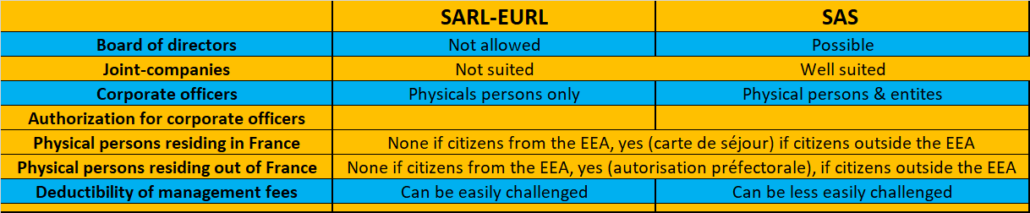

To sum up, below is a summary of the pros and cons of each status when creating a subsidiary in France.

The Jean-Claude ARMAND and Associates firm assists you in the selection of the most suitable choice of legal status when creating a subsidiary in France.