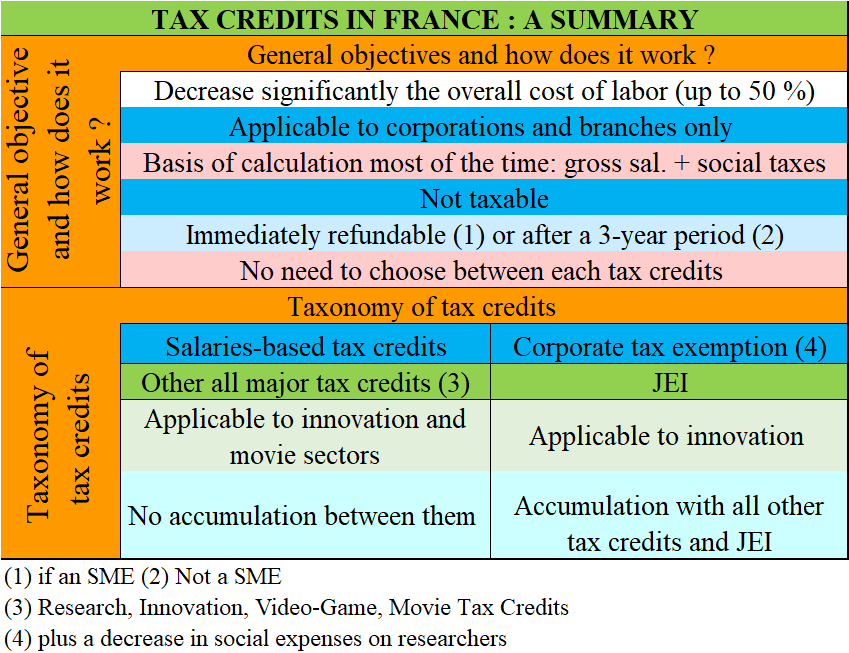

Young Innovative Company Status – JEI : a powerful incentive

Young Innovative Company Status (JEI) – General overview

The status of Young Innovative Company (JEI) enables young companies very active in R&D to get significant financial support to get past the hurdle of the first and most difficult years of their development. It mainly consists in a social expense (tax) exemption on researchers’ salaries and corporation tax exemption as well.

Conditions to acquire the JEI status

To acquire the JEI (Young innovative company) status, the company must fulfil 5 conditions:

- Be less than 8 years old,

- Be an SME according to the General Tax Code,

- Be independent (at least 50% directly or indirectly owned by physical persons, including venture capitalists),

- Practice an authentically innovative business,

- Dedicate at least 15% of the total company’s spending in R&D,

The calculation of R&D’s share of expenses is roughly the same as the research tax credit (CIR).

To preserve its status, the company must maintain all these requirements for each fiscal year.

Subsidiaries of groups can benefit from the statuts if they were pre-existing companies. However, subsidiaires newly incorporated by groups are not eligible for it.

Exemptions granted by the Young Innovative Company Status

Companies that obtain the JEI status benefit during the eligible period of 3 types of exemption:

- Exemption of employers’ payroll taxes for research personnel salaries over 8 years,

- The following tax relief:

- Exemption on corporate income tax during 12 months over 8 years,

- 50% tax allowance on profits for the following 12 months,

- Total exemption of two local business taxes (C.F.E. and C.V.A.E.)

These tax exemptions on corporate income tax are subject to the European de minimis rule, which sets an upper limit on tax relief that a company can receive each year. These aids cannot exceed 200 K€ by company over a 3-year period.

Employers’ payroll tax exemptions are capped:

- For each researcher, to the portion of revenue up to 4.5 times the SMIC (minimal French pay) of the gross salary, which represents today €8,108 per month in 2025,

- For each establishment, up to 5 times the social security’s annual (that is €€235,500 for the 2025 calendar year).

How to optimize & secure the Young Innovative Company status?

To reduce the risk of queries from the tax authorities on the innovative nature of the research program, and consequently the JEI status, it is highly recommended for companies to request from the Service des Impôts des Entreprises (SIE) “Corporate tax department” to which they file, to take a stand on the innovating nature of the project(s) by filing a prior notice request (rescript). The absence of an answer from the Administration is worth agreement of its part. However, it can still control the reality and the amounts of the expenses.

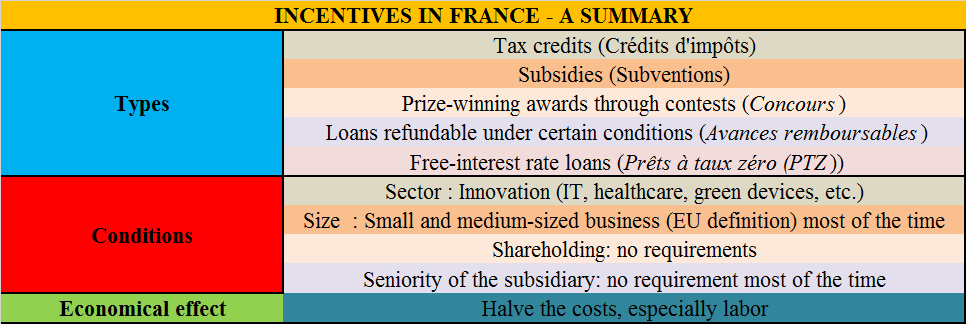

Accumulation of the JEI status with other exemptions or subsidies

The company can accumulate the JEI status with the CIR (research tax credit), innovation and employment subsidies.

THE YOUNG INNOVATIVE STATUS – IN BRIEF

Young Innovative Company

Our flexible and lean organization relies on experts and tax lawyers, who master the English language (and in some cases German) and have a confirmed experience of CIR. We assure you a quality of service comparable to that of large consulting firms, but at much lower rates. At Jean-Claude Armand and Partners, we consider that tax advantages should benefit above all the companies. For us, this is fundamentally a question of ethics!

Need more information?

: how to take advantage of it? Summary")