Short-term rentals and RSI: Should you abandon the flat rate taxation?

Abstract – Short-term rentals and RSI

Do short-term rentals and the RSI mean a substantial increase in your tax and social security contributions? This is what was feared with the lowering of ceilings and allowances under the flat-rate system from January 1 2024. But it was not adopted. However, this lowering will be probably enacted in 2025. This postponement is an opportunity to consider the switch to the simplified tax regime (régime simplifié d’imposition (RSI)). Paradoxically, whatever your sales figures, this system can reduce your tax and social security contributions compared with the flat-rate system even though you are a non-resident in France. Here’s how it works.

Short-term rentals and RSI:

What legislators had to change in 2024…

To encourage investors to switch to long-term rental, the legislator had made a distinction between tense and non-tense zones for seasonal or RBNB renters. In the 1st category, the sales threshold below which the lump-sum scheme could still be applied was to be lowered from €188,700 in 2023 to €77,700 in 2024, and the deduction on revenues from 71% in 2023 to 50% in 2024. In non-tensioned zones, this same sales figure of €188,700 was to be lowered to €50,000, and the tax allowance rate was to remain unchanged at 71%.

…And what’s changed in 2024…

On the other hand, the Finance Act 2024 has, retroactively to January 1 2023.

- For unclassified furnished tourist accommodation lessors, lowered the ceiling and allowance from 77,700 and 50% respectively to €15,000 and 30% (cf. article 50-0 of the General Tax Code (CGI) 1° and 2° b).

- An additional 21% allowance has been created for renters of furnished tourist accommodation in rural areas.

Short-term rentals and flat-rate taxation – summary

Short-term rentals and RSI:

What are the consequences if you exceed the thresholds?

If you exceed the applicable thresholds, you are automatically taxed under the simplified tax regime (RSI), in the BIC category. In other words, your income is the difference between earned income and earned expenses. Earned income means income and expenses generated during the year in question. The fact that these revenues and expenses were not received or disbursed during the year in question is irrelevant. In other words, you are required to keep (or have kept) accounting records on an accrual basis and are no longer taxed on a percentage of your income.

Is it very penalizing in terms of taxation?

Short-term rentals and RSI are not necessarily a penalizing combination. Recording actual expenses can result in an expense ratio of over 50%, or even 71%. In particular, you can deduct (i) depreciation on real estate assets, (ii) transaction costs on said assets and (iii) URSSAF contributions (as long as your acquired (or realized) sales exceed €23,000 in a full year). Better still, you may discover that you should have abandoned the flat-rate tax regime long ago ….

And what about social security contributions?

With the switch to the simplified tax system, you can no longer contribute based on a percentage of sales. Instead, you contribute on the basis of your actual taxable profit. And unlike the flat-rate system, these URSSAF contributions are tax-deductible (see paragraph above). You will be subject to them only if your turnover exceeds €23,000.

What if I sell a property after switching to the simplified tax system?

- You are a non-professional (that is your turnover does not exceed €23,000)

- Capital gains are subject to the personal income tax regime (régime des particuliers).

- You are a professional (that is your turnover exceeds €23,000)

- Regarding income tax, capital gains are subject to the system for professional capital gains. However, under certain conditions, you may be exempt from taxation.

- The capital gain corresponding to the depreciation deducted for tax purposes is subject to URSSAF contributions. This is the case even if you are exempt from taxation (see above paragraph).

Short-term rentals and RSI – Example of a comparison with the flat-rate system

The data

Consider a “loueur en meublé professionnel” – one of our customers – with the following characteristics:

Sales €90,000 entirely in classified meublés de tourisme.

External expenses

Council tax: €2,317

Property taxes: €3,408

Condominium charges: €4,410

Electricity: €3,300

Internet: €1,510

Miscellaneous fees: €2,900

Non-occupant owner insurance (PNO) : €576

Platform commissions: €15,250

Miscellaneous expenses (small materials and equipment): €3,500

Janitors: €29,000

Interest: €4,740

URSSAF contributions (including regularization); €679 of which €242 non-deductible CSG/RDS (we will assume that the furnished lettings operator has switched to the actual tax system and pays URSSAF contributions as a self-employed worker from January 1 2023),

Building purchase price: €787,000, 65% of which is depreciable over 35 years (the land, estimated at 35% of the price, is not depreciable),

Purchase price of fixtures and fittings: €44,700 amortized over 12 years.

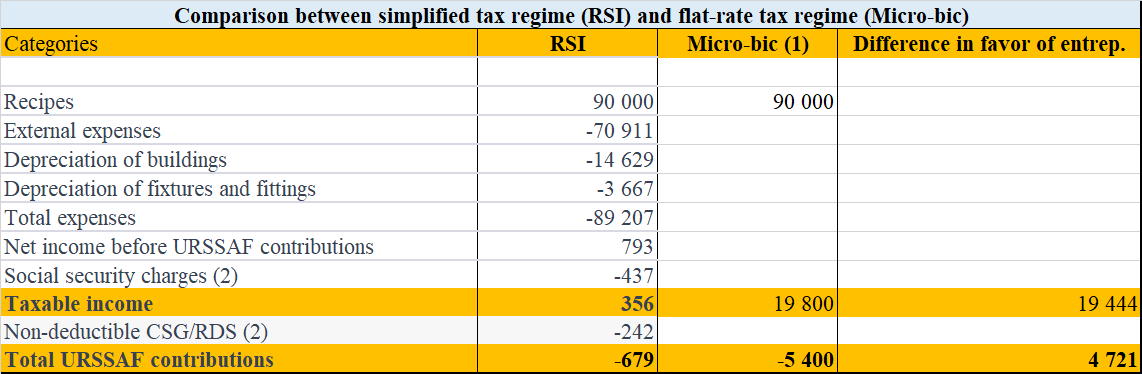

Summary Comparison of RSI and flat-rate tax system

As a result, the actual taxation system allows our customer to reduce

- His/her personal income tax base of €19,444,

- His/her URSSAF contributions of €4,721.

Short-term rentals and RSI

(1) Micro-bic: taxable income €90,000 x (1-71%); URSSAF contributions: €90,000 x 6%.

Short-term rentals and the RSI are a win-win situation: our customer should have switched to the real tax system at least as of January 1 2023!

Jean-Claude Armand et Associés can help you make the transition from flat-rate to simplified taxation regime (RSI).